I’ll be talking about the Registered Education Savings Plan or RESP today. Hurray! That’s one of my favorite portions of Personal Finance and Investing. We all love our kids, they are the future. We slog for them day and night working hard and dreaming big for them. So, why not invest in RESPs and secure their future? They’ll be thankful to you for this, If not, that’s ok they are still our kids.

BTW, RESPs just like RRSPs (Registered Retirement Savings Plan) have tax benefits as well. Can you please answer this simple question for me – What do tax benefits and saving for post-secondary education have in common?

That’s easy, it’s an RESP – that is a Registered Education Savings Plan. The name doesn’t sound as appealing as what it promises, especially for people who couldn’t be further from financially savvy or money talk.

We all have kids, we love them. We work for them, care for them, and dream about their future all the time. As a kid, I’ve always looked up to my parents, learning from them, reading with them, playing around, and most of all – they are my parents (they protect me from any storm ahead, making me secure and strong). RESP is one such instrument you should invest in. They are great financial instruments and the Canadian Government is excellent at adding a top-up to your investments every year, which will propel the growth that much faster.

Not to forget, TD e-Series mutual funds are some of the best in the market in terms of market returns and capital growth. You may want to Google and read on Reddit, TD e-Series funds are always the most recommended especially for your children’s RESPs. In fact, even we have invested in the TD e-Series for our son who is 6 now.

If you have a child under college age, having an RESP is the best way to significantly lessen the financial cost of your child’s higher education. Let’s get started. Buckle up your seat belts now!

What Is An RESP?

There’s a lot to like about this registered investment account. Its most immediate benefit is the fact that the money that goes into it is tax-sheltered. Granted, your RESP contributions are not tax-deductible, however, they are not taxable either. You only pay tax on the interest on your contributions.

What this means is that if you put in $100,000 and contribute $3,000 to an RESP, your personal income tax will only apply to the $97,000 left. Also, say your contribution accrues interest resulting in a total of $3250, you only pay tax on the $250 interest; your original contribution of $3000 remains un-taxable.

Also, unlike a TFSA or an RRSP, an RESP has no yearly contribution limit. You can put in as much money as you want to in one contribution although that is not a good idea, but more on that in a minute.

What Is The RESP Contribution Limit?

An RESP has a total contribution limit of $50,000 per child/beneficiary, and while you can have an unlimited number of plans per child, the total contribution across all the plans for each child still has to keep to the $50,000 limit.

Another fun feature about the RESP is that you do not have to make the contributions alone; the way it is structured allows others to pitch in and contribute to your child’s higher education. It could be anyone: close friends and neighbors, a favorite uncle or aunt, grandparents, and more.

Now, concerning the reason why large RESP contributions are a bad thing.

When you make your contributions gradually, the government matches your contribution by up to 20% of $2500 annually through the Canadian Education and Savings Grant. What this means is that if you contribute $2500 yearly, you stand to receive up to $500 from the government every year.

If you contribute more than that every year, your government RESP grant will still top out at $500.

However, the lifetime contribution assistance you can receive from the government is $7200, so make sure to spread out your contributions enough for you to take full advantage of that grant money.

How To Open An RESP Account?

You can open a Registered Education Savings Plan (RESP) for your child as soon as he/she is born and start contributing to the account from that moment.

Usually, parents/guardians will contribute to this account until the child is up to 18 years old or ready for college. Once the child is ready for university education, he/she begins to receive periodic payments from the RESP. These payments are called educational assistance payments (EAPs).

An RESP is valid for receiving contributions for 36 years after it is opened. However, if for some reason, your child does not attend a university or a trade school, within that time period, you will have to return the government’s contribution to them.

Alternatively, if you have more than one child, you can always transfer the RESP from one child to the other if the original recipient decides against any form of higher education.

You must note that with this investment account, the money saved and earned with it can only be used for education-related expenses. If you use the funds for anything otherwise, your expenses will incur income tax as well as a 20% penalty.

What Are TD e-Series Mutual Funds?

It is one thing to have money in an RESP for your child and shelter it from tax; it is quite another to know how to grow that money. Since an RESP is an investment account, there is only one thing to do with its funds – invest.

Like other types of investment accounts, an RESP can hold a vast number of investment products: ETFs, bonds, stocks, mutual funds, and more.

Traditionally, people have opted for mutual funds because of their low investment cost. The Management Expense Ratio (MER) is typically much lower (0.33% – 0.55%) than for actively traded equity mutual funds with MERs over 2.00%. For any investor, this is a huge saving on investment fees.

TD Bank has proven to be a leader and a forerunner for this kind of investment product. And previously, you could only get the TD e-series mutual funds directly from the bank. You had to either open a mutual fund account with the bank or via their discount brokerage option, TD Direct Investing.

Thankfully the process has been made easier by the fact that you can now purchase the TD e-series mutual funds directly from other discount brokerages at no trading cost.

How To Open a TD e-Series Funds Account?

Opening a TD e-Series account would be the next logical step to take for investing with your RESP contribution. Although TD’s e-Series lineup has performed over the years, they have never been too good at providing concise detail about opening an e-Series Funds Account.

Hopefully, this page on their website can help you with all the information you need. To put it simply, these are the general steps you should take when you go into ay TD branch for this purpose.

-

Be specific about wanting to open a TD Mutual Funds Account

-

You will be provided with an investor profile questionnaire (Customer Information Profile) that you should fill thoughtfully with the help of an advisor

-

You will then need to fill out and sign the forms for the account application. This will include the Understanding and Consent Form

-

Prepare your account to receive pre-authorized contributions directly from your bank account. You will need to provide a void cheque here to facilitate this step

-

Next, make sure you ask for your TD mutual funds account to be converted to a TD e-Series Funds Account

-

You will then be able to access your TD e-Series account online by visiting TD EasyWeb

Recent Changes To The TD e-Series Mutual Funds

While TD e-series mutual funds have been one of the most inexpensive investing options out there, TD Bank made some changes to that affected lineup of e-series funds that have so far proven to be generally positive. You should know of all these changes before you opt for these mutual funds for your RESP investing.

The biggest change is that the TD e-series switched to TD-specific ETFs, tracking slightly different indices as a result (benchmark indices tracked now come from the German index provider, Solactive).

Before these changes, all TD e-series funds were known to hold a collection of standalone bonds and stocks. With this change, these funds now hold TD ETFs instead. These investment products have an even lower MER (approximately 0.05% lower) and will drive investment costs down even further.

The Best TD e-Series Funds To Save For Your Child’s Education

So now that you know the relative benefits of investing in TD-specific ETFs, how would you invest your RESP money to make the most of it before your child is ready for college? We will lay down here for you some of the best options from the TD e-series lineup that you can put your money on.

These options will vary slightly in the indices they track, their Management Expense Ratio, their asset mix, and their risk level. But bear in mind that they are all built for investment success.

Also, the MERs here are not yet the new fees that are expected to be 0.05% lower.

Top 7 TD e-Series Mutual Funds

Alright then, straight to the list now. Here’s the list of the top 7 TD e-Series Mutual funds you should buy for your children’s future:

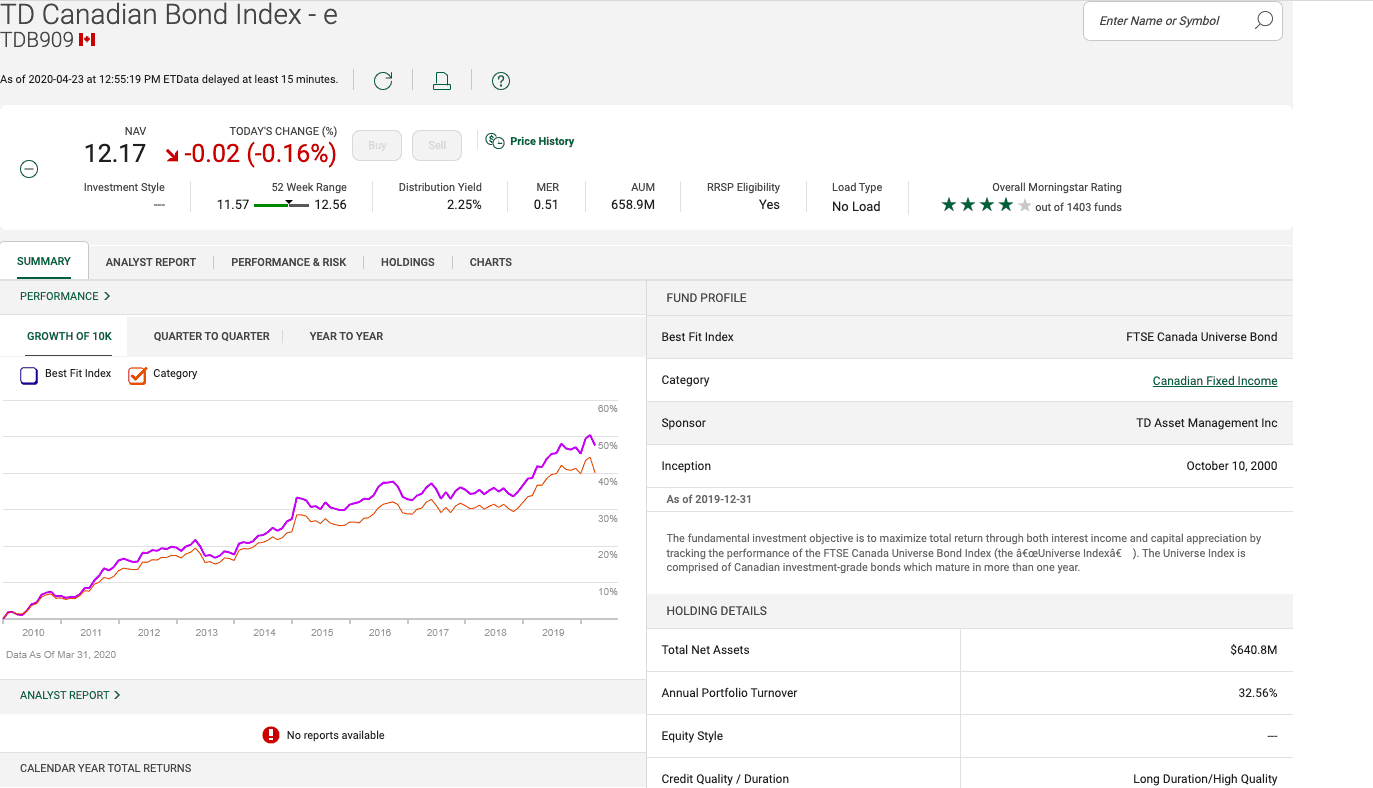

1. TD Canadian Bond Index – e (TDB 909)

The benchmark index for this ETF is the Solactive Broad Canadian Bond Universe TR Index. There is no asset mix here as all the money put in this ETF is focused on bonds.

This 100% bond ETF has a Management Expense Ratio (MER) of 0.50%. And based on its other features and its overall positioning, the TDB 909 is a low-risk investment.

This makes it perfect for investors with a lower risk threshold who would rather have a guaranteed profit, no matter how little.

-

TDB 909 tracks Solactive’s Broad Canadian Bond Universe TR Index

-

Attracts a Management Expense Ratio (MER) of 0.50%

-

An asset mix that is 100% focused on bonds.

-

It is a low-risk investment

Click here to view more details about this mutual fund

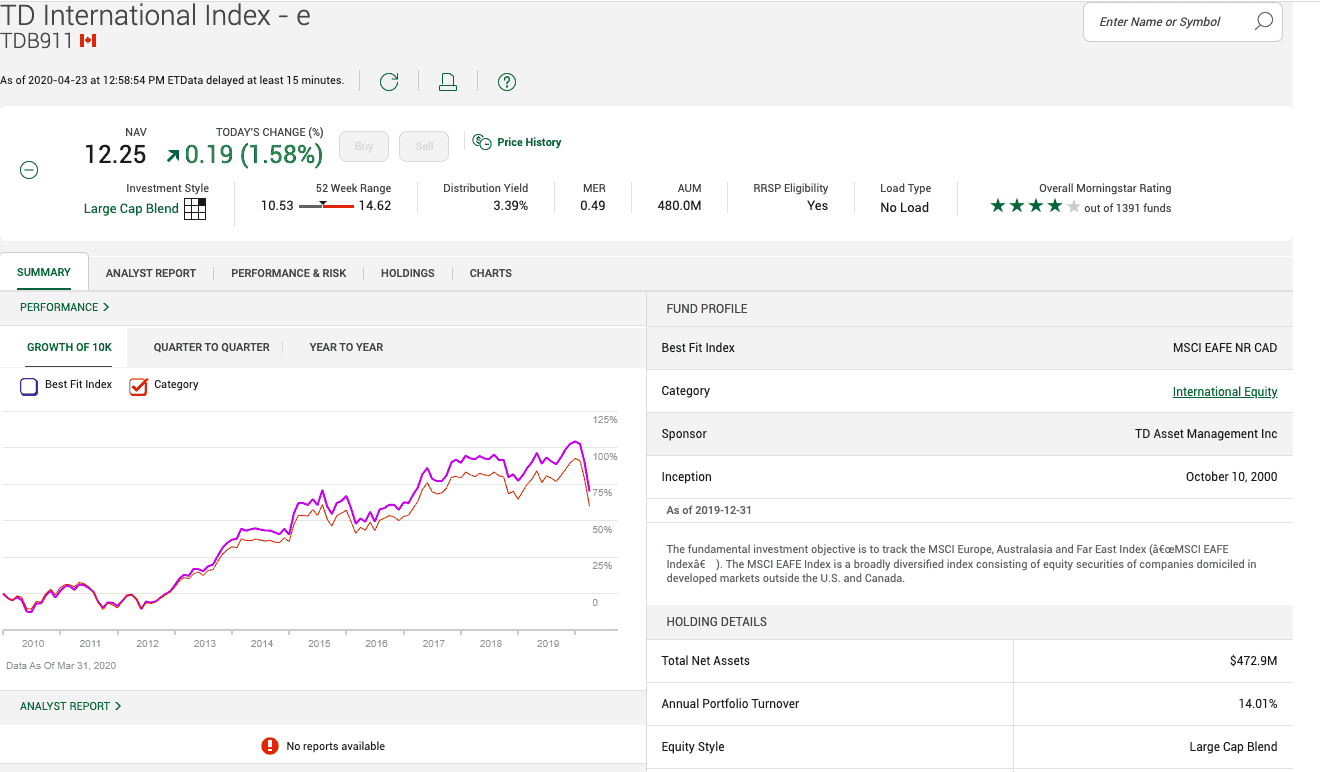

2. TD International Index-e (TDB911)

This ETF is a little riskier than the TDB 909. This TD ETF keeps an eye on the Solactive GBS Developed Markets example – North America Large & Mid Cap CAD Index.

In terms of asset mix, the TDB 911 is almost entirely made up of international stocks. The international stock percentage stands at 99% with the outstanding 1% being made up of income trust units.

Like the TDB 909, the International Index-e has a Management Expense Ratio (MER) of 0.50%. If you don’t mind opening up your RESP contribution to a little more risk for the sake of a little extra in earnings, this is worth considering.

-

TDB 911 tracks Solactive’s GBS Developed Markets ex-North America Large & Mid Cap CAD Index

-

Attracts a Management Expense Ratio (MER) of 0.50%

-

Has an asset mix that constitutes 99% international stocks and 1% income trust units

-

It is a medium-risk investment

Click here to view more details about this mutual fund

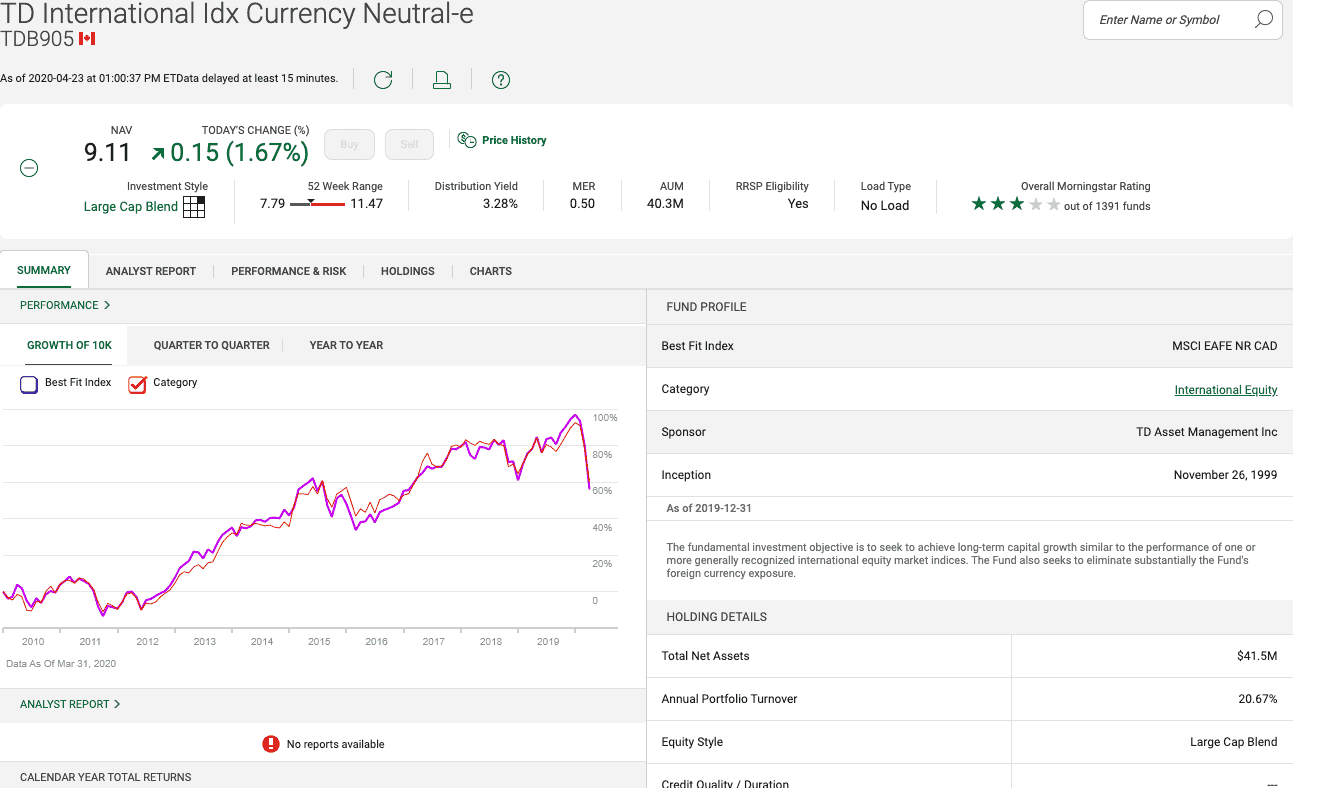

3. TD International Index Currency Neutral-e (TDB905)

Our third ETF on this list keeps an eye on the Solactive GBS Developed Markets ex North America Large & Mid Cap Hedged to CAD Index.

With a Management Expense Ratio of (0.51%), TDB 905 is made up of 97% of international stocks, 1% income trust units, and 15 cash and equivalents.

Like the TDB 911, this ETF is an alternative for those with a mid-level risk threshold.

-

TDB 905 tracks Solactive’s GBS Developed Markets ex North America Large & Mid Cap Hedged to CAD Index

-

Attracts a Management Expense Ratio (MER) of 0.51%

-

Has an asset mix that is made up of 97% international stocks, 1% income trust units, 1% cash and equivalents

-

It is a medium-risk investment

Click here to view more details about this mutual fund

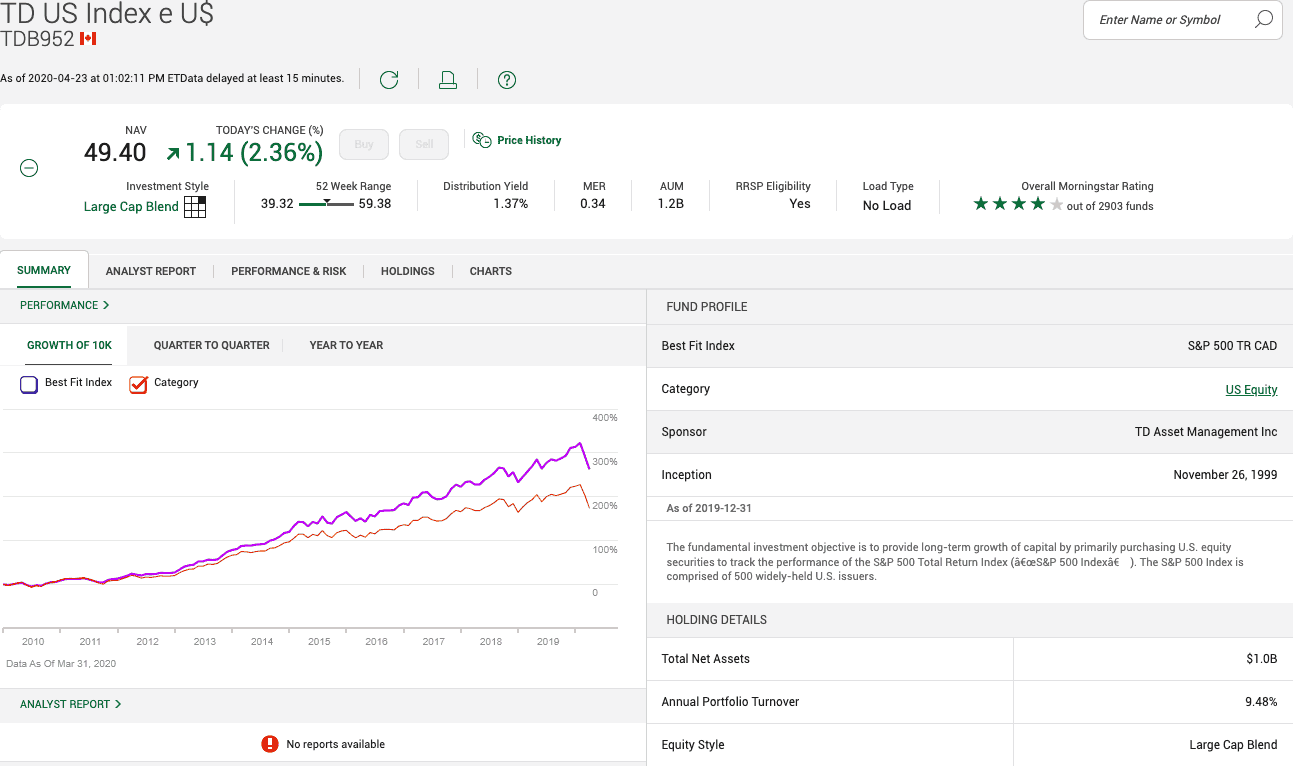

4. TD US Index Fund (US$) e- (TDB952)

The ETF with the lowest MER so far on this list – it has a Management Expense Ratio of 0.35%. The TDB 952 gets its cue from the Solactive US Large Cap Index. Its asset mix is slightly varied from what you get when investing in TDB 905.

Here, the asset mix is split into 97% US stocks and 3% international stocks. Also considered to be in the mid-level risk threshold, the TD US Index Fund (US$)-e is wonderful for stock lovers who are always looking for even lower investing fees.

-

TDB 952 tracks Solactive’s US Large Cap Index

-

Attracts a Management Expense Ratio (MER) of 0.35%

-

The TDB 952 asset mix contains 97% US Stocks and 3% international stocks

-

It is a medium-risk investment

Click here to view more details about this mutual fund

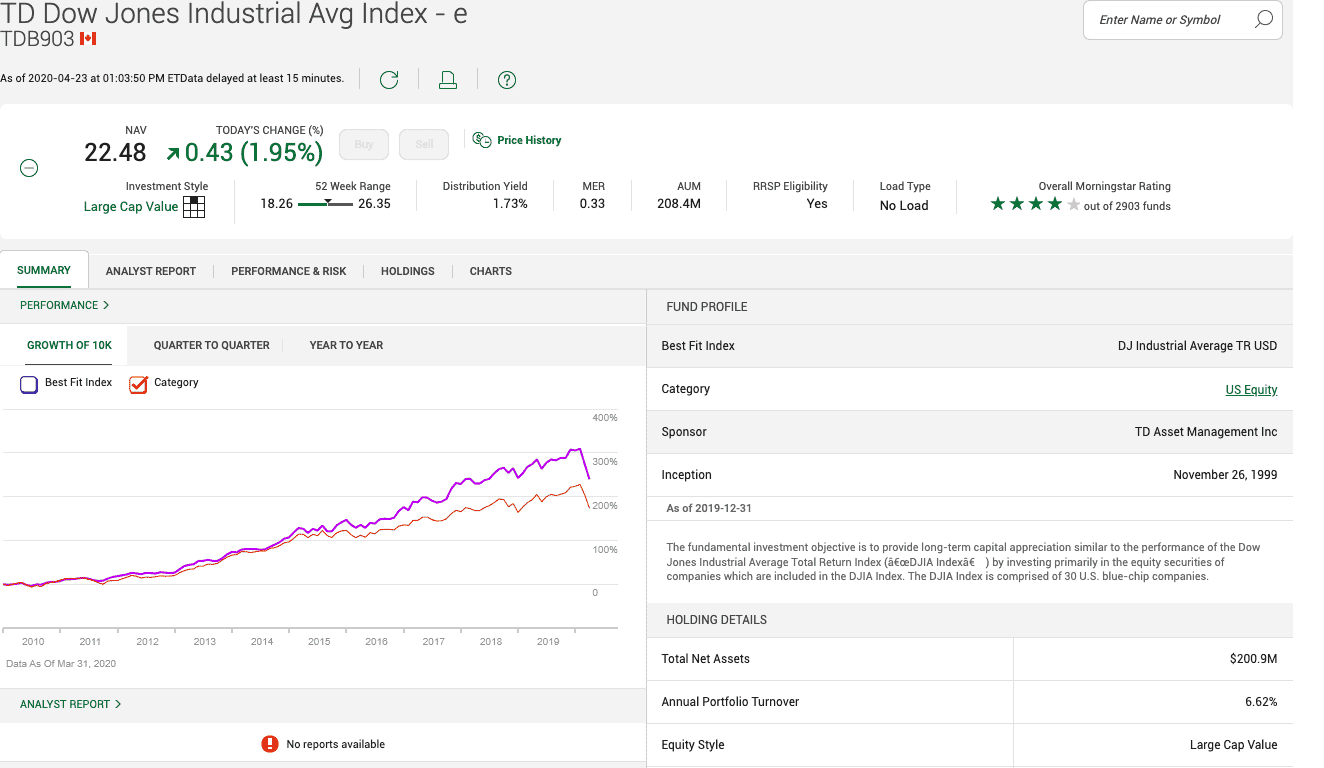

5. TD DJIA Index – e (TDB903)

The lowest investing fee percentage yet on this list, the TDB 903 incurs a Management Expense Ratio of 0.33%.

Also for the medium risk investors, the TD DJIA Index-e’s benchmark index is the DJIA Total Return Index US$. The only asset here is stocks, so all investments are 100% put in stocks.

-

TDB 903 tracks DJIA Total Return Index US$

-

Attracts a Management Expense Ratio (MER) of 0.33%

-

There is no asset mix. The ETF is 100% made up of stocks

-

It is a medium-risk investment

Click here to view more details about this mutual fund

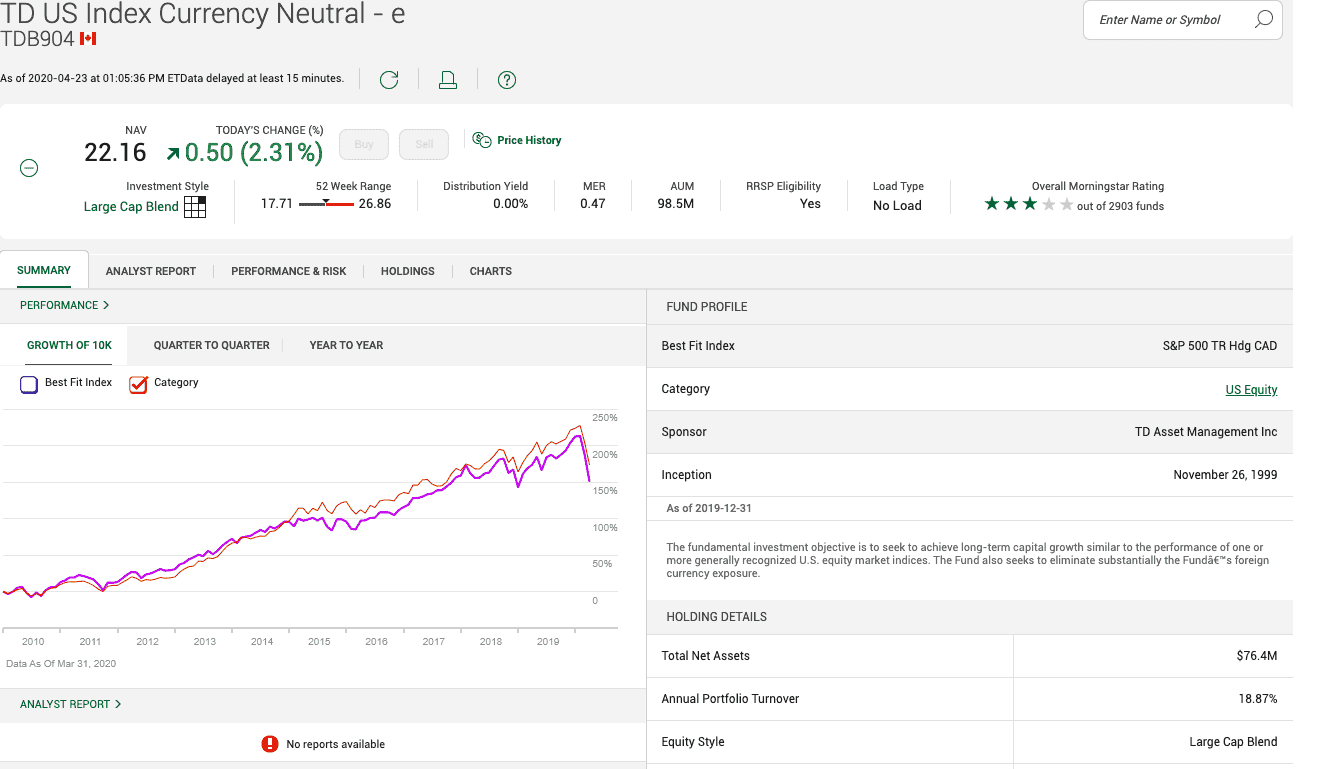

6. TD US Index Currency Neutral Fund – e (TDB904)

TDB 904’s has Solactive’s US Large Cap Hedged to CAD Index as its benchmark index. It has a 0.50% Management Expense Ratio (MER).

This TD ETF is an investment mix that is 2% cash and equivalents, 2% international stocks, and 95% US stocks. It is another good option for those with medium risk tolerance and a particular affinity for stocks from US companies.

-

TDB 904 tracks Solactive’s US Large Cap Hedged to CAD Index

-

Attracts a Management Expense Ratio (MER) of 0.50%

-

Has an asset mix that is made of 95% US stocks, 2% international stocks, and 2% cash and equivalents.

-

It is a medium-risk investment

Click here to view more details about this mutual fund

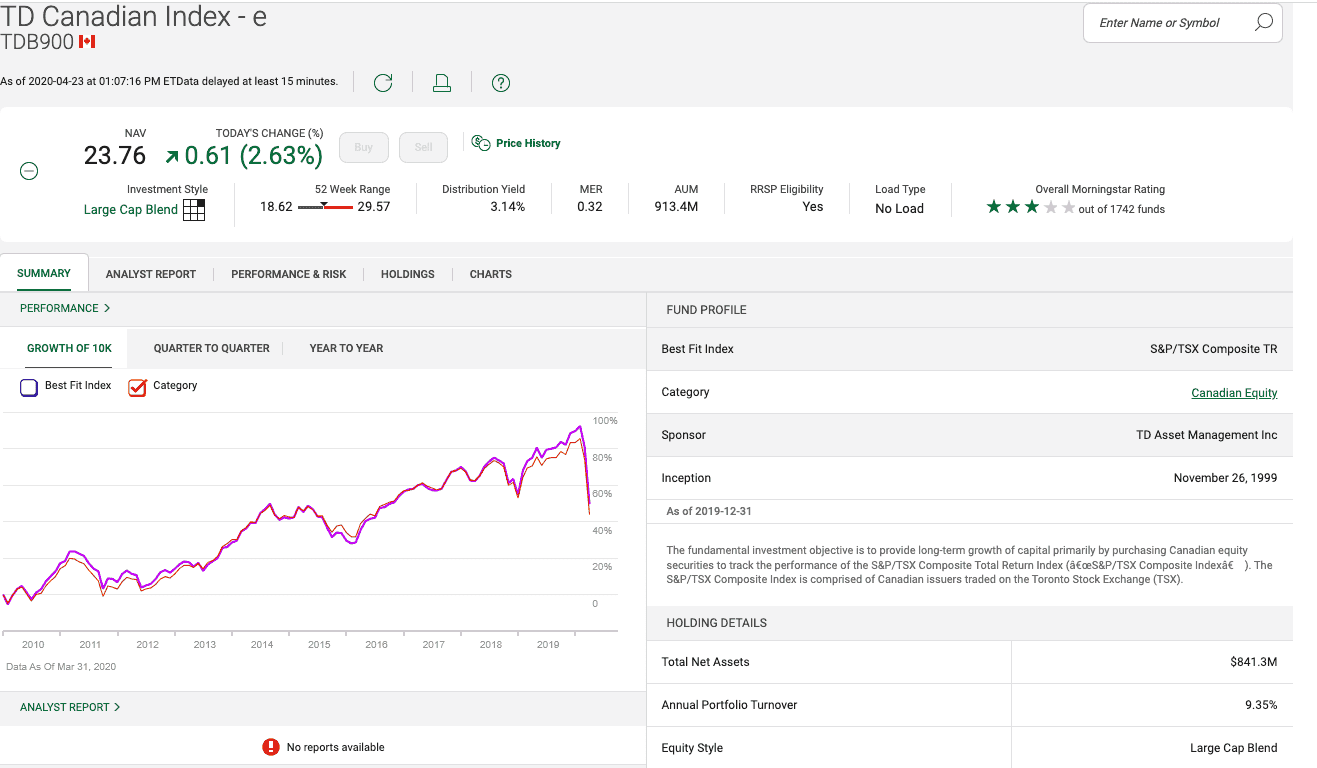

7. TD Canadian Index-e (TDB900)

TD’s TDB 900 has one of the richest asset mixes of its entire TD e-series lineup. It also has an attractive Management Expense Ratio (MER) of 0.33%.

The TD Canadian Index-e has the Solactive Canada Broad Market Index (CA NTR) as its benchmark index.

When it comes to asset mix, TDB 900 is made up of 96% equity, and 4.65 income trust units. Its equity percentage is further broken into 95% Canadian stocks, 0.1% US stocks, and 0.20% international stocks of the entire asset mix.

The TDB 900 is ideal for patriotic investors; that is investors who prefer to put their money on Canadian stocks.

-

TDB 900 tracks Solactive’s Canada Broad Market Index (CA NTR)

-

Attracts a Management Expense Ratio (MER) of 0.33%

-

Has an asset mix of 96% equity (95% Canadian stocks, 0.1 US stocks, 0.20% International Stocks) and 4.6% of income trust units

-

It is a medium-risk investment

Click here to view more details about this mutual fund

How To Rebalance Your RESP Portfolio?

One of the most important practices for any investment portfolio is to learn to periodically rebalance your portfolio.

Due to a few factors, chief of them being market uncertainly, your carefully planned fund mix can begin to drift, leaving you with more shares in one fund than you want to own. This can throw off your entire investment and plunge you into unexpected losses if you leave them unattended.

So what to do? Make sure that you rebalance your portfolio every so often, preferably twice a year or at the end of every year at the least.

Rebalancing your portfolio simply implies resetting the asset mix so it goes back to its original allocation and back on track to hit your intended investment targets.

You can do this in two ways: you can either add the required amount of money to the investment, specifically to the underperforming assets to reset them to the original allocation.

Alternatively, if you do not have any money to inject into the portfolio, you can sell off some shares from the better-performing assets and put that money into the underperforming ones to bring them back up to par.

This second option is basically you selling high and buying low, which is a common-sense investing strategy.

Conclusion

TD e-Series funds remain a top indexing choice for couch potato investors who do not have the stomach for active investing.

For those investing for their child’s education, your time frame, investing goals, risk tolerance and more will differ depending on your unique situation, and this will affect your decision to opt for TD’s offering or to find an alternative.

Although the TD’s e-Series lineup is definitely worth considering (especially with the new updates), they may not be your best bet.

You owe it to yourself to check out other investment options like Tangerine Funds, Wealthsimple, or trading ETFs with platforms like Questrade. At the end of the day, the point of it all is that you invest.

If you like the content you just read and find it helpful, please do me a favour and share this post on social media and help spread the word. Also, let me know your thoughts and comments in the comment box below. That’s all for now. Stay Healthy and Stay Safe. Bye now!