CPP payments are a monthly, taxable benefit that you receive when you retire from active work. CPP payment dates fall in the last week of the month except for December when it is paid on the 22nd.

CPP, basically, acts as social security for lifelong income after active service or work. In case you don’t know, CPP payments are not paid automatically. It requires you to meet certain criteria and make regular contributions towards it, the advance of the time you wish to start receiving it.

The Canada Pension Plan (CPP) is open to all residents of Canada except those who reside in the province of Quebec. Quebec offers its residents a special pension plan known as the Quebec Pension Plan. There are various pension plans in Canada including the Canada Pension Plan (CPP), Old Age Security Pension (OAS) and Registered Pension Plan (RPP).

The Canada Pension Plan (CPP) is a retirement pension benefit that is paid by the Canadian Government to eligible individuals. The money paid is determined by how much you have contributed during your years of employment and how long the contributions were made for.

In this article I’ve covered everything about the Canada Pension Plan (CPP), CPP Payments Dates for 2021, How to apply for CPP, How much CPP you’ll get and so on and so forth. Let’s get started.

What Is The Canada Pension Plan (CPP)?

The Canada Pension Plan is a government-sponsored retirement pension income plan, which is engaged with the responsibility of paying retirement or disability benefits.

The Canadian Pension Plan (CPP) was established in 1965 in order to provide a basic benefits package for retirees and disabled individuals.

In the province of Quebec, a provincial plan known as the Quebec Pension Plan has been put in place for its workers.

The age to start receiving CPP is 65. To be eligible to receive CPP Payments, you must have worked in Canada and regularly made CPP contributions. CPP payments are not automatic. You must apply before you can start receiving the CPP pension benefits.

All Canadians, including those working outside Quebec, must contribute to CPP payments as long as you earn more than the basic exemption amount.

Contributions are mandatory for workers below age 65 and voluntary for those past 70 years. CPP payments are paid out monthly and twelve times in a calendar year. I’ve mentioned the CPP Payments Dates for 2021 below.

CPP Payment Dates In 2021

The Canada Pension Plan (CPP) retirement amount is paid on a monthly basis.

In case you don’t know – survivor, dependent’s, disability, and retirement payments are all done in the same period.

CPP payments can be requested via a direct deposit into your bank account. However, those of you that prefer a paper cheque may have to wait for at least a week for the payment to process.

Below is the CPP Payment Dates For the fiscal year 2021:

-

January 27, 2021

-

February 24, 2021

-

March 29, 2021

-

April 28, 2021

-

May 27, 2021

-

June 28, 2021

-

July 28, 2021

-

August 27, 2021

-

September 28, 2021

-

October 27, 2021

-

November 26, 2021

-

December 22, 2021

The above-mentioned CPP Payment Dates are also applicable to the CPP retirement pension income, CPP Disability payments, Children’s benefit and survivor’s benefits as they are paid out on the same date.

Requirement To Receive The CPP Payments?

To qualify for the CPP Payments, the basic requirements include:

-

Age: You must be at least 60 years old

-

Contributions: You are required to make regular contributions to the plan

-

You must have worked in Canada for a period of time

-

You must apply within 12 months of when you wish to start receiving the payment

Contribution Rate For CPP Payments

The contribution rate for CPP is 5.25% (10.50% if self-employed) on incomes ranging from $3,500 to $58,700 in 2021. If your income is $3,500 or below, you won’t contribute to CPP and for those that earn $58,700 and above CPP is also not contribute.

The maximum CPP contribution for employers and employees is $2,898.00 each.

When a person retires, the benefits they receive are determined by the number of years they contributed for. The Canada Pension Plan is paid monthly. It is designed to cover about 25% of the contributor’s earnings. CPP benefits are taken to be taxable income.

Eligibility For CPP Payments

The CPP is an earning-based social program designed to protect Canadian workers and their dependents against the loss of income. Contributors must meet all of the following criteria to qualify for the Canada Pension Plan.

-

You must have worked in Canada for a while and have contributed at least once to the CPP

-

You must be 59 years and above and be approved by a Canada Service Center near you

Your eligibility for the CPP benefits begins in the first month of your 65th birthday. Contributors can wait until their 65th birthday to receive their full benefits or opt to receive them earlier on their 60th birthday.

However, that would mean that your benefits will be slightly reduced. Contributors can also choose to delay their benefits until their 70th year, as this can grant an automatic increase in their benefits.

How Do CPP Payments Work?

The CPP amount paid to you on retirement is usually based on three significant criteria, which is your average income throughout your period of working, your contributions to the CPP Payments and the age you decide to start receiving the retirement pension.

You can start receiving your CPP Payments from 60, however, the standard age is 65 years and to increase your monthly amount.

This means that I can apply for my pension at age 60, but my monthly amount will be small, however, if I wait till I’m 65, the CPP payment amount will increase and the maximum amount will be reached by the age 70. This increase or decrease in the amount is permanent.

For 2021, the maximum amount is $1,175.83 monthly and the average monthly amount is $679.16.

Remember, it is important to apply for the CPP pension as the payments are not automatic!

CPP Pension Sharing

CPP also makes provision for pension sharing among spouses or common-law partners and also parents who had to take a lesser paying job or cut back on hours, during their period of contributions, to take care of children below the age of seven years.

Pension sharing requires that you and your spouse or common-law partner live together and it is cancelled when there is a voluntary separation between you two. The portion of your pension that qualifies for sharing is based on the period of time you’ve lived together during your joint contributory period. Pension sharing has you and your partner to save on tax, as CPP retirement pension is a taxable income.

How To Apply For The CPP Payments?

As earlier stated, the CPP payment income is not an automatic process. It requires you to apply for the plan, have your application approved and then start your retirement earnings.

CPP payment benefits are not sent to just anyone, even those who are eligible until an application has been submitted. Before you apply, you should have your Social Insurance Number. You can apply for Canadian Pension Plan online.

However, if you are not able to, you can fill out a paper application or mail it to the closest Service Canada centre.

If you fill out the online application, make sure to print out the signature page of the application, sign it, and mail it to Service Canada.

It usually takes about 7 to 14 days for online applications to be processed and 120 days for applications mailed to Service Canada Centres.

Here are some important things to know when applying for the Canada Pension Plan

-

You must have your Social Insurance Number (SIN) and bank information handy

-

You shouldn’t apply if you’re not ready to start receiving your retirement pension

-

The maximum time for application is 12 months before the date you wish to start receiving the payments

-

Application Methods: You can either apply online through their “My Service Canada Account”, mail or at a Service Canada Centre. These methods of application take different lengths of time to process. The online application takes 7 to 14 days, applications delivered at a Service Canada Centre takes 120 days and those sent through mails also take 120 days to be processed

-

If your application is denied, you can make an appeal through the Canada Pension Appeals Board

What Is The CPP Application Process?

Receiving CPP retirement benefits does not start automatically. Contributors must apply for it.

While contributors can apply for their CPP retirement pension online, there are exceptions, such as if you have authorized someone else to access your account, if you reside outside Canada, or have already earned some benefits due to disability or retirement.

You can email the nearest Service Canada Center or print out a paper copy if you can’t apply for the CPP retirement pension online.

How To Contribute To CPP Payments?

The CPP contribution you are required to make is a certain percentage of your earnings. If you have an employer and earn more than $3,500 per annum, you are required to contribute up to 5.25% of your income, with the maximum amount being $2,898.00.

Your employer must also contribute a matching amount annually. For the self-employed, you are required to contribute 10.2%, which is $5,796.00. These amounts are based on the yearly maximum pensionable earnings, which is adjusted each year to take into consideration the cost of living and the inflation rate.

The current maximum pensionable earnings for CPP is $58,700 and the minimum is $3,500.

This means that the maximum amount you and I can be taxed on, as individuals, is $55,200.

If you are between the ages of 60-65 and you decide to continue working while receiving your CPP payments, you must continue to make contributions to the pension fund. This means that your CPP contributions are mandatory at all times.

If you’re a 65-70-year-old already receiving the CPP payments and still employed, your CPP contributions are voluntary. You can decide whether or not you wish to continue making contributions.

Your CPP contributions will be directed towards your post-retirement benefits, which will increase your retirement monthly income. However, you cease making CPP contributions once you hit the 70-year mark whether or not you’re working or self-employed.

How Much Should I Contribute To CPP Payments?

Canadian workers earning more than $3,500 are supposed to contribute 5.1%of their income. Their employers are also obliged to contribute a similar amount each year.

The maximum amount that an employed Canadian should contribute to the CPP payments should not exceed $2,748.90. Self-employed Canadians, on the other hand, should contribute $5,497.80.

The minimum income threshold for contributing to the Canada Pension Plan hasn’t changed since 1996; however, the maximum pensionable income has been increased to cater for inflation and the cost of living.

The annual maximum pensionable income in 2019 was $57,400, which means the maximum taxable income cannot exceed $53,900. Canadians aged between 60 to 70 years can continue to work and contribute to their CPP payments, which will be allocated for post-retirement benefits.

Whether you are employed or self-employed, your contribution to the CPP payments ceases typically at the age of 70.

How Much Will I Get From CPP Payments?

CPP payments you’ll get depends on factors such as the amount you’ve contributed to the CPP pension and for how long.

Your contribution period begins typically at age 18 and ends at the 70th birthday or when one passes away. If you start contributing to the CPP pension payments below the age of 65, you can expect to incur a 0.6% reduction each month until your 65th birthday.

Your CPP reduction will be approximately 36% if you begin contributing at the age of 60.

However, delaying your CPP payments can attract a 0.7% increase each month up to your 65th birthday (or 8.4% per year). It is often difficult to estimate the amount payable, given that there are so many factors that are involved.

Canadian workers often consider the following factors before deciding when to receiving their CPP payment benefits.

-

Your savings, company pension plan, or investment

-

Your disabilities and family health history

-

How much you have contributed to the Canada Pension Plan and for how long

-

Your age

-

Whether you plan to continue working while receiving retirement pension or not

-

Whether you earn any other income such as rental income or business investment

The Canadian government has provided its citizens with the average maximum pension amount to help them in planning for their retirement. Receiving CPP payment benefits does not start automatically. Contributors need to apply for an access code and set up an account.

Here’s how much you can expect from CPP Payments:

| CPP Retirement Pension (at the age 65) | $735.21 | $1,175.83 |

| Post-retirement Benefit(at age 65) | $8.78 | $29.40 |

| CPP Disability Benefit | $1,010.26 | $1,387.66 |

| Post-retirement Disability Benefit | $505.79 | $505.79 |

| Survivor’s pension – 65 years and below | $455.20 | $638.28 |

| Survivor’s pension – 65 years and older | $306.83 | $705.50 |

| Children of Disabled CPP contributors | $255.03 | $255.03 |

| Children of Deceased CPP contributors | $255.03 | $255.03 |

| Death Benefit(one-time payment) | $2,491.89 | $2,500.00 |

| Combined CPP Payment Benefits | ||

| Combined Survivor’s and Retirement Pension (at age 65) | $897.87 | $1,175.83 |

| Combined Survivor’s CPP pension amount and Disability benefit | $1,148.56 | $1,387.66 |

What Is CPP Pension Sharing?

The law allows Canadians to apply to share their CPP pensions with either their common-law partner or married spouse. However, the sharing partners must be eligible for CPP pension.

The sharing of CPP benefits can provide some tax savings. Your CPP pension starts once the government approves your application, and it can’t be backdated. The CPP pension amount depends on the number of months or years you and your partner or spouse has been contributing. The law requires married couples to submit their marriage certificate as part of the CPP sharing application.

Your CPP payment contributions can be divided equally after a divorce or separation.

CPP Payment Benefits

The Canada Pension Plan (CPP) includes pension benefits such as:

-

Post-Retirement Pension

-

Survivor’s Pension

-

Disability Pension

-

Death Benefit

-

Children’s Benefit

1. Post-Retirement Pension: These are the benefits paid to you if you continue to work and make CPP payment contributions, while collecting CPP retirement pension, before age 70. This benefit increases your overall pension. This benefit is not eligible for pension sharing.

2. Survivor’s Pension: The partner of a deceased contributor may be eligible to receive a monthly survivor’s pension. For 2021, the maximum CPP survivor’s pension is $638.28 for those below 65 years of age and $705.50 for those over the age of 65.

3. CPP Disability Pension Payment: This benefit is paid to CPP contributors who suffer from a prolonged or permanent disability. They may also qualify for a post-retirement disability benefit.

4. Death Benefit: This is a one-time payment made to the estate of the deceased contributor. The maximum amount that can be paid is $2,500.

5. Children’s Benefit: This benefit is paid to dependent children of a deceased or disabled CPP pensioner. This benefit requires the recipient to be under the age of 18 or under 25 if in school full-time. This benefit is paid monthly and the maximum amount is $255.03. These are payments made monthly to the dependent children of a disabled or deceased CPP contributor. The children must be under 18 or not older than 25 and enrolled as a full-time student in a recognized school.

CPP Disability Payments

For the calendar year 2021, the maximum monthly CPP disability pension amount is $1387.66 .

You will receive the basic monthly amount of $505.79 which is fixed and standard for all CPP payment recipients, and in addition to the basic monthly amount, you will receive an additional amount based on how much you’ve contributed to the CPP during your entire working career.

If you are already receiving CPP disability benefits payment then your dependent children may also be eligible for a children’s benefit. In 2021, the flat monthly rate your child will receive is up to $255.03.

CPP Disability Payments are not necessarily permanent and forever supplement. It is intended to partially replace your employment income for as long as you cannot work on a regular basis. Once you start working on a regular basis, the payments will stop.

Your CPP disability payments will stop if:

-

you are capable of going to work on a regular basis

-

you are no longer disabled and deemed ok

-

when you turn 65 years

-

your death

When you turn 65 your CPP disability payments will automatically be converted to a retirement pension. You do not have to apply for the retirement pension again. Another important point to note here is that your retirement pension will always be less than your CPP disability payment pension amount.

If CPP disability payments are cancelled, any of the related children’s benefits will also be cancelled automatically.

What Is The CPP Survivor’s Pension?

So what exactly is the Canadian Survivor Pension? Who is eligible for this?

In the event of death, the Service Canada Center will take a portion of your CPP pension amount and transfer it to your common-law partner or married spouse.

Survivors who are above 65 years will only receive a portion of the deceased’s CPP payments. However, the survivor will also receive a small percentage plus a flat rate of the CPP pension amount if he or she is below 65 years.

The surviving partner or spouse must apply for the deceased’s premium, and that should be done as soon as death has been reported. Delays can result in loss of some benefits, given that back payments can take up to 12 months to complete. So please be careful here.

Unfortunately, survivors cannot apply for the deceased’s pension online. You have to print out the survivor’s benefit form and email it to the Service Canada Center near you.

Canada Pension Plan comes as a helping hand for Canadians who find retirement planning as overwhelming to them. With a CPP payment, planning for your retirement is fast, simple, and easy.

How To Calculate Your CPP Payments?

To be frank, it is pretty easy to calculate your retirement income and CPP payments. There’s nothing wrong with knowing this amount in advance and planning ahead of time.

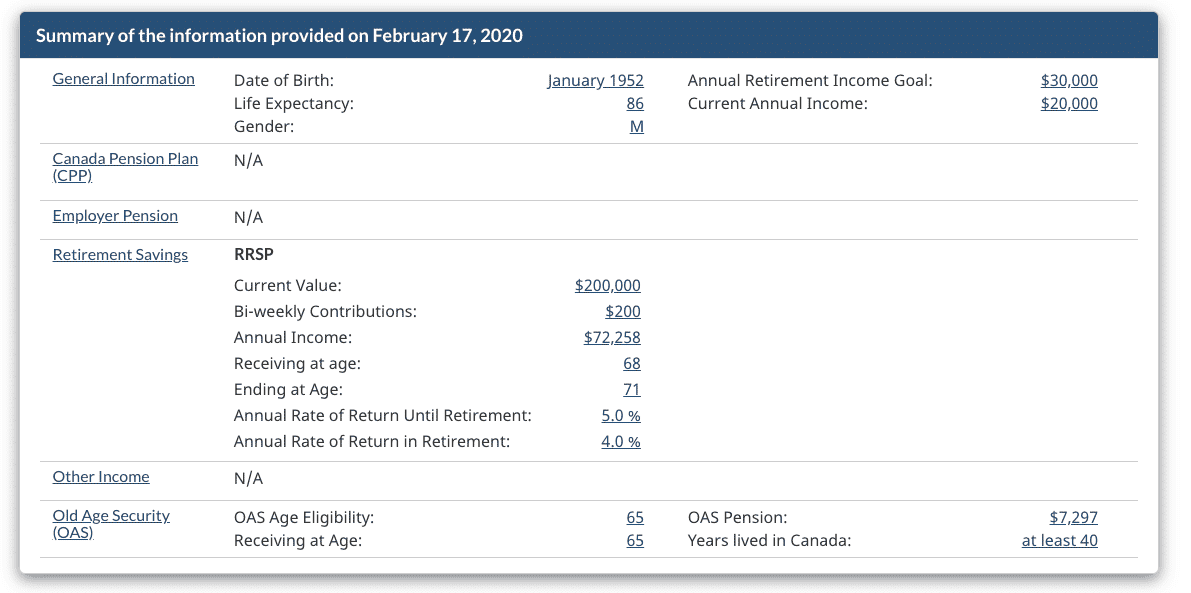

All you have to do is head over to this link. Fill in the basic details which hardly takes 5 – 10 minutes and boom you are done with the report.

This is what you can expect at the end of filling in the details:

Like I said before, you just have to key in the basic details like Year of Birth, RRSP contributions, Annual Retirement Goals etc. and the system will estimate your retirement income, CPP Payments and OAS Benefits you’ll receive.

CPP Payments FAQs

1. What is the maximum CPP pension for 2021?

The maximum monthly CPP payment amount for 2021 is $1,175.83, which translates to an annual pension of $14,109.96.

2. At what age can I start receiving my CPP pension?

CPP payments can be applied for in advance of your 60th birthday, but your monthly pension will be decreased by 0.60%, monthly. However if you wait till you’re 70years old, your monthly pension will be increased by 0.70%, monthly. The standard recommended age to start receiving CPP pension is 65 years.

3. What happens to my CPP pension after I die?

After death, your CPP pension will be paid to your legal spouse or partner, children or into your estate as survivor’s benefit, children’s benefit or death benefit.

4. Will I still receive my CPP pension if I relocate to another country?

Yes! You will still receive your monthly pension regardless of where you relocate to. However, if the country you now live doesn’t have a tax treaty with Canada, your pension is liable to a 25% tax rate. On the other, tax rates are reduced or waived, if the country has a tax treaty with Canada.

5. How many years do I need to work to get CPP Payments?

You’re entitled to CPP payments regardless of how long you’ve worked. the most important variables in your Canada Pension Plan are your earnings and how much contributions you make to the CPP.

Final Words

There you go, that was all about the Canada Pension Plan (CPP). Canadians refer to the Canada Pension Plan as a pillar of their retirement income. It guarantees contributors and their dependents a steady flow of income after retirement, death, or disability.

A pension plan is, basically, a retirement plan that requires you or your employer to put aside a certain percentage of your annual income in preparation for your retirement.

If you like the content of this article and find it to be helpful, please share it on social media and help spread the word. Also, do let me know your question, thoughts and comments below. Thanks for reading and have a fantastic day!

Top 10 Popular Posts Of All Time