Tattooed Chef (TTCF) looks to be promising for the long-term haul. Let’s see why.

The Tattooed Chef is a plant-based company that sells frozen foods in retailers like Costco, Walmart and Sams Club. The US frozen food market is worth about 55 billion and the Tattooed Chef is trying to disrupt the market with quality foods that are plant-based. A big part of this change is coming through the Millennial generation and Generation Z.

The average millennial and Gen Z cannot cook, so what do they do take out and frozen foods. But with more of a focus on vegan and plant-based foods. This is where the Tattooed Chef comes out to shine.

The average man spends close to $300 at the grocery store and for women, it’s even more at $323.

How large is the Millennial and Z generation in America you ask? 133 million Americans large and if they spend per se 20 dollars each for frozen foods that are plant-based based. That is around 2.6 billion USD of revenue for the TTCF.

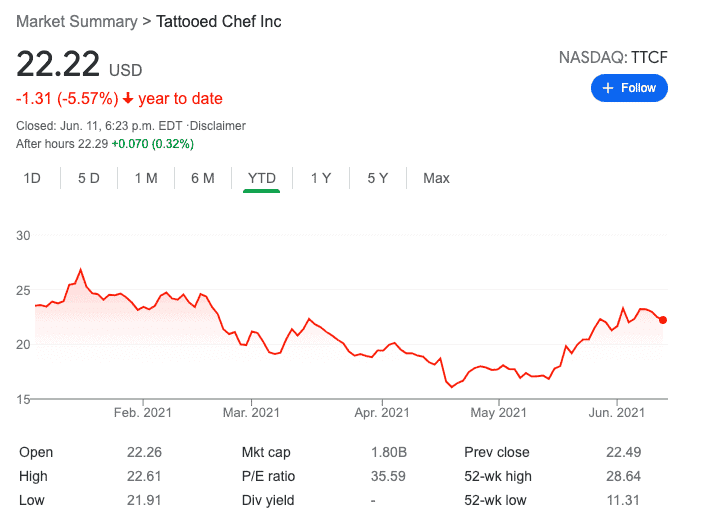

TTCF Stock Price

Currently, the stock trades at $22.22 USD, as of close on Friday.

Just in case you don’t know, TTCF trades on the NASDAQ with a market cap of 1.80B. Year to date the stock hasn’t done much in terms of price movement, almost staying flat between 20 – 30 USD.

Tattooed Chef stock does not pay any dividends currently. (It neither has paid in the past)

What does the Tattooed Chef have that the Very Good Food Company and Beyond Meat BYND doesn’t?

Well, The ability to have innovative products with a potential of 62 SKUs in 2021 and they are targeting around 200 SKUs.

Also, Tattooed Chef is vertically integrated meaning that they own all forms of manufacturing and idea-sharing. They can go from an idea to market in 3 days (now, that’s brilliant).

Remember, Tattoed Chef has all types of frozen foods in their product line up such as Single-Serve Bowls, Smoothie Bowls, Vegetable Blends, Meat alternatives and Plant powered Pizzas. They also have launched a European commerce site as it will draw in new customers from all over the US.

The company currently has around 200K space of manufacturing room. But it is important to note that they have doubled the space in 2020 and will again double in 2021 (manufacturing room).

Also, The company is ramping up production as they are on target to reach 62 different SKUs. They have a plant in Italy and a plant in California. The Italy plant will especially be good for the European expansion in 2024. Their Certifications are on another level they have all of the organic seals approved from the USDA.

Tattooed Chef Revenue Forecast

Tattooed Chef Revenue increased 87% year o year from 2019 to 2020. They went from 58.1 Mil to 108.9 Million in 2020.

Also, their gross profit increased 70% from 9.9 Million to 16.8 Million in 2020. The adjusted EBITDA went up from 4.7% with a percentage of sales of 8.1%. It went up to 10.6% of total sales of 9.7%. They have not launched their Ad council yet but it should again help with total sales.

The predicted revenue for 2021 is 222 million which is almost a 100 percent raise of revenue.

In 2022 their revenue should be around 300 million with a Gross margin of 25 – 30%.

By 2023, the revenue should be at 500 million with a total margin of 30 to 35 %.

2026 is the killer year with a predicted revenue of 1 billion with total margins of 35% plus. The adjusted EBITDA should be 20 % as of 2026 and in 2021 it should be in the main teens.

As of Q3, 2020 Tattooed Chef had total assets of 66.718 million with 56.550 million of total liabilities. They recently exercised a warrant for 230 million worth of cash and it puts them at 296,718 million USD. Their P/S is about 13.04.

The company has a forward P/E of 309.25. Based on the above statics with a P/S of 13.04 and with a 2021 revenue of 222 million their market cap should be 2,894,88 Billion which is almost a Billion more in market cap. My price target 12 months from now should be 45-50 USD.

Tattooed Chef (TTCF) Forward-Looking and Price Targets

Tattooed Chef is currently valued at about $1.8B (market cap).

-

With 2023 Revenue guidance at $500m and an extremely conservative P/S (Price to sales) of 5 (Remember, BYND (Beyond Meat) is about 25) suggests a $2.5B valuation and a 40% return from current levels. 15 P/S is more realistic – suggesting a $7.5bn market cap and over a 400% return.

-

Tattooed Chef also has a 155% growth in points of distribution, with projections to grow to over 200% in 2021 alone. They are looking to expand beyond the US market

-

Vertically integrated operations reduce costs massively and impact margin positively.

-

The E-commerce side of the business has started to operate recently.

-

8% of shares are held by institutions (when this gets covered more we should see share price shoot up).

-

The company hasn’t really spent anything on advertising yet and is pulling in huge numbers. They are planning on going all out on advertising in 2021.

Thanks for reading let me know your thoughts and comments below.

Top 10 Popular Posts Of All Time

- Top 30 Canadian Blue Chip Stocks You Should Own

- How To Use A My Service Canada Account

- How To Watch Free TV Shows In Canada – List of 10 Best Sites

- VGRO Review – Vanguard’s Best Growth ETF Portfolio

- Top 7 Canadian ETFs You Should Own

- Top 150+ Dividend Stocks In Canada – Complete List

- Credit Karma Canada Review – Free Credit Score And Report

- CPP Payment Dates – How Much CPP Will You Get?

- Top 5 High-Interest Savings Accounts In Canada

- How To Open A CRA My Account?