If you are a resident of Canada, you have probably come across the term Tax-Free Savings Account or TFSA. Many financial institutions are prone to advertising these accounts to their customers.

If you have heard of a TFSA account before and have always remained on the fence, unsure whether to open one or not then rest easy. This article will tell you exactly what TFSAs are, including the contribution limits and room.

While the government encourages you to save money through the TFSAs and RRSPs, not many Canadians make use of this opportunity.

Canadians held a total of $276.7 billion in their tax-free savings accounts in 2017, with the average TFSA holder holding $19,633, according to statistics released by the Canada Revenue Agency (CRA) Friday.

Let’s get started.

What Is A TFSA?

As the name implies, TFSA is a tax-free savings account in which the contributions, earned interests, earned dividends, and all gains on capital are not taxed. What’s more, withdrawals can also be made from the TFSA account tax-free.

Unlike the regular savings accounts, TFSAs can hold cash as well as other forms of deposits. You can contribute to a TFSA in form of securities, bonds, or mutual funds.

According to the CRA, there were 19.5 million TFSAs in 2017, held by 14.1 million TFSA holders, for an average of 1.38 accounts per holder. That was up from 18.3 million TFSAs in 2016, held by 13.5 million TFSA holders, for an average of 1.36 accounts per holder.

If you are considering opening a TFSA account, then there are three types of TFSAs to choose from. You can either open an annuity contract account, a deposit account, or have a trust arrangement. These accounts can be opened with any eligible Canadian financial institution (Banks, Credit Unions, etc.)

Source: Wealthsimple

How Do TFSAs Work In Canada?

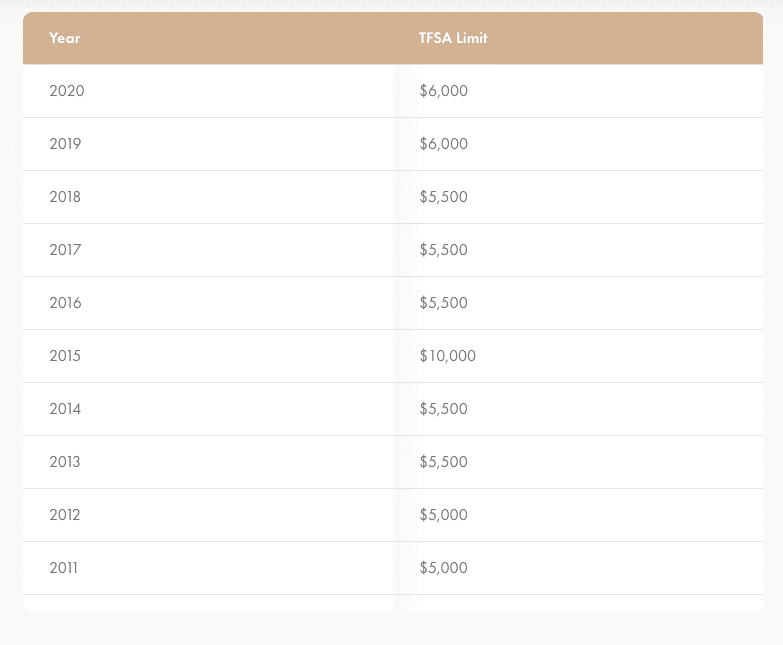

TFSAs were first introduced in 2009.

During the initial days, TFSA accounts had the contribution limit set to $5000 annually.

TFSA limits have changed over the years increasing from $5000 to $10,000 in 2015, before settling at $6000 in 2019.

For the year 2021, the TFSA contribution limit is set $6000. This value might change in the coming year (i.e. 2021) or remain the same. It’s all up to the CRA (Canada Revenue Agency), the arm of the government in charge of setting the TFSA limits.

According to the RBC survey recently, 57% of Canadians hold an active TFSA account while 52% hold the RRSP account.

TFSAs work by letting you earn interest on all your contributions without being taxed. This is the one trait that sets it aside from most other savings account in Canada.

Take for instance, if two account holders, A and B, both decide to save $6000. A decides to save in a TFSA while B saves in a regular investment account. If both earn an annual interest of 7% on their funds, the total amount at the end of the year is $6420.

When A makes a withdrawal from his TFSA, the interest earned on his contribution will not be taxed. B on the other hand will end up being taxed on the $420 interest on his initial deposit.

What Are The Requirements for Opening a TFSA account?

With the impressive advantages of the TFSAs, it’s hard to imagine not wanting to open one. So what are the requirements for opening the TFSA account in Canada?

First of all, TFSAs are only available to Canadian residents older than 17 years (18 years and up.) It is also important that you have a valid SIN. Without this, you’ll not be eligible to open a TFSA.

It is noteworthy that if you are considered a non-resident Canadian for one reason or the other, you can still be eligible to open a TFSA if you have a valid SIN.

The only difference is that all your TFSA contributions will be subjected to a penalty. This penalty is usually a 1% tax on your monthly contributions.

Click here if you want more information regarding the non-resident situation.

Also, you will not be allowed to open or contribute to a TFSA until you turn exactly 18. So until then, you are not considered old enough to open a TFSA. Once the date passes, you will be allowed to open the account and contribute to the set annual limit.

To clarify, if you turn 18 on the 23rd of October 2021, you cannot open a TFSA until the 23rd of October. Once it’s 23rd of October you will be considered eligible to open an account.

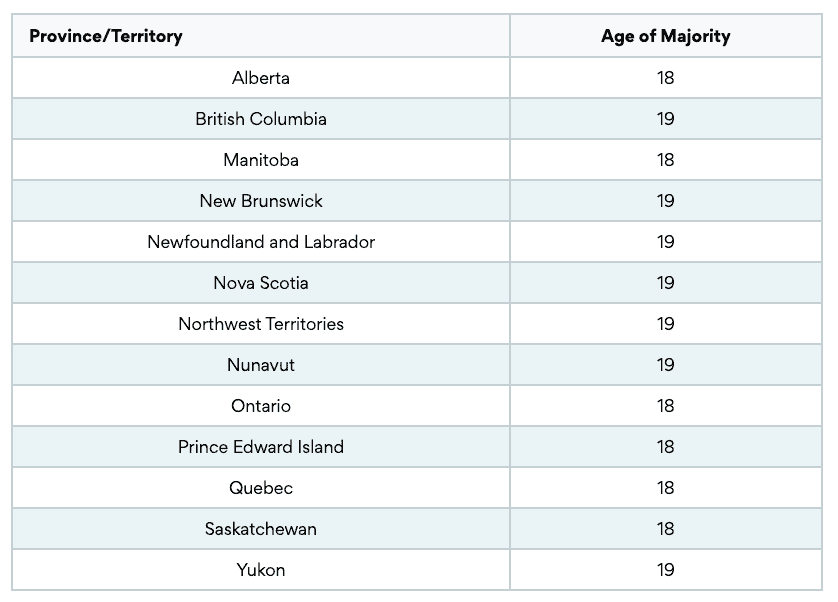

It should also be noted that the legal age in some provinces is 19 years rather than 18 years.

Individuals younger than 19 years in these areas are considered too young to enter into a contract, thus are ineligible to open a TFSA. Once they turn 19 years old, individuals in these areas with a valid SIN can open a TFSA.

Source: ratehub.ca

How To Open A TFSA?

Once you fulfill both the age and SIN requirements, you can open a TFSA. Note that while the account can be opened at any time during the year, the annual contribution limit must still not be exceeded.

To open a TFSA make sure you follow these two simple steps:

-

Reach out to your preferred financial institution. This can be a credit union, a bank, or even an insurance company.

-

Give the financial institution or issuer, your date of birth as well as your SIN. This will allow them to register you for a TFSA. In some situations, your issuer may request for certain documents.

Try to provide accurate and correct information to your issuer. Otherwise, your registration may end up being nullified and denied. This translates into any income you earn being recorded on your Income Tax and Benefit Return.

You can also choose to open a self-directed TFSA. This is for those who prefer to manage their investments on their own. If this option suits you, contact an issuer for more information on self-directed TFSA.

Luckily, Tangerine Bank is currently offering a special offer exclusive to open a new TFSA account.

Tangerine TFSA Account Features:

-

Account Interest rates: 2.50% (promotional for the first 5 months); 0.15% after 5 months

-

Minimum deposit: None

-

Transfer Fees: $50

-

TFSA Accounts are eligible for CDIC coverage

You can open a new TFSA or RRSP account today with Tangerine and get a special interest rate of 2.50% for the first 5 months. After the initial 5 month period, you’ll earn the regular interest rate of 0.15%.

Click here to open your Tangerine TFSA Account today and get the special promotional rate of 2.5% daily interest. (Offer valid for a limited time only.)

Remember it doesn’t cost you a penny to open the Tangerine TFSA/RRSP account, and there is no annual maintenance fee.

In case you’re looking at opening a new RRSP Account, the same promotion applies, click here to open a new RRSP account for FREE with Tangerine Bank! There are no annual fees or annual maintenance fees at Tangerine.

How To Invest in TFSAs?

In the TFSA account, you can invest in Mutual funds, stocks, real estate, bonds, doesn’t really matter. The important thing to always remember is, your money Inside a TFSA will grow tax-free – be it dividends received or the capital growth.

You should make the choice of your investments based on two main factors:

-

Your tolerance for risk: how much risk are you willing to bear? Make deposits in terms and forms of this.

-

Your investment horizon: this relates to how soon you will need to access your funds.

Putting these two in mind and combining them with what other factors surrounding your situation will guide you to make the best choice for you when contributing to a TFSA.

How To Contribute To The TFSA?

A contribution room is a maximum sum that you can contribute to a TFSA.

While this might seem to limit you at first, it actually affords quite a bit of flexibility. Contribution rooms accumulate for all the years after 2009, that you were living in Canada while 18 (19 for some provinces) or older.

So any contribution room that has been left unused, can be transferred into the next year.

Take, for instance, if you only contributed $2000 out of the allowed $6000 back in 2019, you can contribute an additional $4000 to the limit for 2021. Your contribution room for 2021 will thus be $10,000.

TFSA contribution room accumulates even for the year where you haven’t made any contribution at all.

Say, for example, if you haven’t contributed to a TFSA since 2016 and you were 18 and older, then your TFSA accumulated contribution room will be $23,000 as of today. This takes into account the varying contribution limits for all the previous years.

Any income earned through investments or interests does not affect your contribution room in any way. (or capital gains through investments).

If you want to read more about the TFSA and RRSP Contributions limits, click here.

How To Withdraw From The TFSA?

If you make a withdrawal from a TFSA, the amount withdrawn is added to the following year’s contribution room.

For example, if you contribute $5500 out of the contribution limit of $6000 for the year 2021, and withdraw $2000 you cannot make another deposit that would put your account over the annual limit. You’d only be allowed to deposit $500 for the current year.

Then at the beginning of the following year, $1500 will be added back to your TFSA contribution room to cover for the rest of the withdrawal from the previous year.

Simply put, regarding contributions and withdrawals, there are just two rules to keep in mind.

One, do not go over your contribution limit. If you do you will be taxed 1% of the excess for every month till you withdraw it.

Two, understand how contribution rooms work. Withdrawals do not automatically open up your contribution room. TFSAs contribution limits stay the same all year long, so you will have to wait till the following year to redeposit your excess withdrawals.

Limitations Of TFSAs

TFSAs might be pretty awesome but if you aren’t cautious, you might end up in some trouble with the Canadian government.

How?

Well, there are no limits on the number of TFSA accounts you can open. This could also cause you to lose sight of how many TFSAs you are making contributions to. Once you over-contribute, either intentionally or by mistake, you will receive a 1% tax penalty on the excess amount in your TFSA.

This might seem pretty easy to avoid, but it is also quite easy to forget. So keep an eye on all your TFSAs as much possible.

Also, stocks cannot be day-traded in TFSAs. So avoid doing inside the TFSA.

TFSA vs. RRSP

Should you pick investing in the TFSA or RRSP? or Both?

First of all, before we begin, TFSAs are for Tax-free savings while RRSPs are mainly aimed at retirement income.

The two account types (TFSA and RRSP) are quite similar, leading to confusion when picking between the two.

Consider these factors though when choosing between the two

-

TFSA deposits are not tax-deductible while RRSPs deposits will form a part of your taxable income.

-

Any withdrawal you make on an RRSP account will end up being taxed, while TFSA withdrawals will not be taxed.

Technically, if you earn over $50000 annually and are planning to save up for retirement, then a TFSA might not be the best choice for you. RRSPs are much more suited for this purpose.

Otherwise, if you have some extra pile of cash (Inheritance or Bonus) lying around and haven’t put much thought towards saving up for retirement, then a TFSA might be the choice for you. They don’t have any limit on the deductions you can make annually unlike RRSPs.

TFSA contribution room will roll over whereas for the RRSP, it won’t.

For more information on deduction limits, check here.

You can also access the TFSA funds much faster than RRSPs.

So if you want to save up for something more immediate than retirement, then use a TFSA rather than an RRSP. If you do have a tendency of spending your savings, then a TFSA might not be such a great option for you.

If you are already contributing to an RRSP through an employer, you can still take advantage of a TFSA. Neither limits the other and you get access to much better tax savings.

How To Check Your TFSA Limit?

Making sure you’re within the TFSA contribution limit is always better to avoid paying the penalty on the over-contribution.

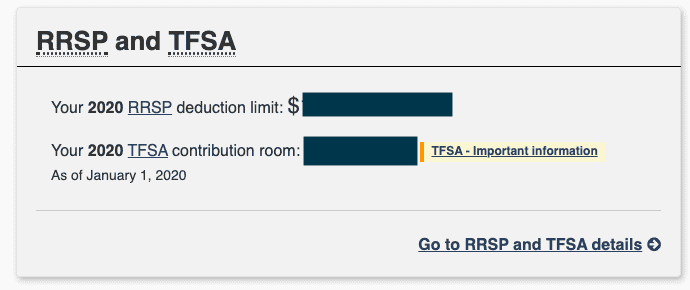

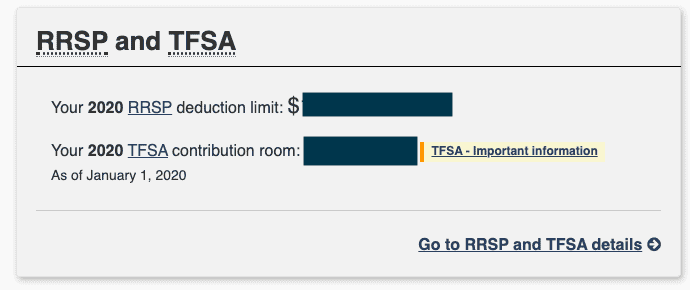

One way to make sure if to login to your CRA My Account page. Here’s how to do it step by step:

-

Login to your CRA My Account. Choose one of two options to sign in.

-

Once in your account page, scroll down and right at the bottom of the page, you’ll see the RRSP and TFSA section.

-

Under the RRSP and the TFSA tab, you’ll immediately see the account limits individually as in the screenshot below.

-

If you need further details, click on the link which says “Go To RRSP and TFSA details”.

- 5. By clicking the above link, you’ll be taken to the TFSA and RRSP page, which will further explain your contribution limits and the date it was calculated on.

What If A TFSA Holder Dies?

No one likes talking about death but sometimes we just have to.

What happens if a TFSA holder dies? Knowing this will let you plan appropriately and avoid stress.

If the TFSA account holder appoints a beneficiary on their account before the death, then the account and all its contents will be transferred over to the beneficiary. This beneficiary could be a spouse, child, or even a common-law partner.

Almost anyone can be a beneficiary to your TFSA Account.

Any income on the account, earned after the death of the original account holder will be sheltered from tax. Take note that if there was an already existing case of over-contribution, this also transfers to the beneficiary’s account.

If the new account’s balance is still within the yearly contribution limit, then there is no problem.

Otherwise, the regular 1% tax penalty on over-contribution will be applied to the beneficiary’s account.

Final Words

TFSA is the best tax free savings instrument in Canada. You can make some fantastic gains within the TFSA and still not pay any taxes on the gains you’ve made. Mind you, in Canada the capital gains tax is almost 50% for non-registered accounts.

So make sure you get the most of your Tax Free Savings Account today.

Setting up a TFSA is not a bad idea. It’s free to do so. However, there might be an account maintenance fee if you don’t maintain the minimum balance.

With TFSAs, not only is your deposits tax-free, but you maintain regular access to your funds at all times.

As long, you do not exceed the yearly contribution limit, then there is no reason to fear.

If you are a low-income earner (below $50000 annually) and are trying to save up funds for a particular goal, whether, for school, a new home, or perhaps even a new car, then TFSAs will be the better place to shelter and grow your funds.

You can open as many TFSAs you want and make deposits. So what are you waiting for? Click here to open a new TFSA account with Tangerine Bank. It is $0 to open, no annual fee, no minimum balance required to maintain or $0 penalties. You’ll get a 2.5% bonus interest rate for the first 5 months. Later on, it is 0.15%.

Thanks for reading. Please let me know your thoughts and comments below.

Top 10 Popular Posts Of All Time

- Top 30 Canadian Blue Chip Stocks You Should Own

- How To Use A My Service Canada Account

- How To Watch Free TV Shows In Canada – List of 10 Best Sites

- VGRO Review – Vanguard’s Best Growth ETF Portfolio

- Top 7 Canadian ETFs You Should Own

- Top 150+ Dividend Stocks In Canada – Complete List

- Credit Karma Canada Review – Free Credit Score And Report

- CPP Payment Dates – How Much CPP Will You Get?

- Top 5 High-Interest Savings Accounts In Canada

- How To Open A CRA My Account?