Do you prefer investing in XEQT (iShares Core Equity ETF Portfolio) or 100% equity Robo Advisor? A Robo is fantastic for investing completely on autopilot. It’s a great option for those looking to set it and forget it. However, there are other advantages and benefits to buying your own ETFs, of course.

First off, Both are fantastic long-term options. XEQT will outperform the Robo advisor given the MER is 0.20% versus the 0.60% (approx) that you’re paying for the Robo. So you’ll have to decide if that’s worth it to you for the automatic set and forget contributions. With an account balance under $100,000, either will do fine. However, my personal preference is XEQT in the long run. Here’s why.

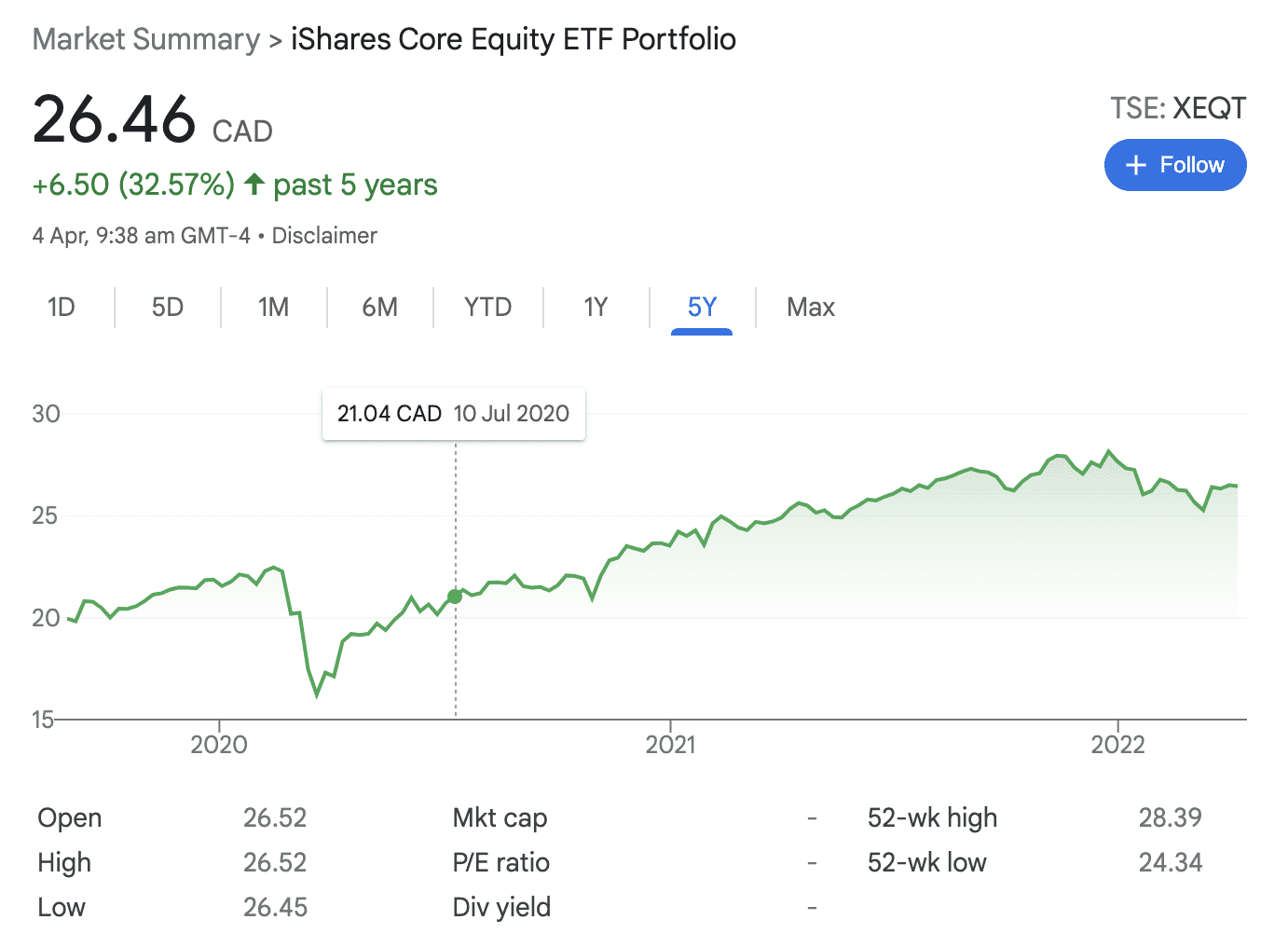

Below is the 5-year chart for XEQT.

In addition, there’s no fee for buying and selling stocks or funds traded on the TSX in Wealthsimple so you’d only be paying the XEQT MER of 0.20%.

It’s 0.5% under 100K contributions and 0.4% above I believe. MER isn’t stacked on top in the sense of you being billed monthly, because it’s embedded in the returns you get from the funds. So you pay both Wealthsimple Invest’s 0.5% fee and the different ETF MERs.

Overall, XEQT will be cheaper but you’ll have to do the buying.

To clarify, whether you use a Robo advisor or not, you’ll pay the MER. The difference is that the Robo buys multiple ETFs and the average MER might be higher than 0.20% (XEQT) which would make the Robo advisor more expensive than manual XEQT. Might also be lower but I doubt it.

Anyways, your timeline for putting money in the market needs to be 5-10 years (long-term investing) at a minimum. If you have 100K to put in, but you know you will need 20K in 2 years, only put 80K in. Do not invest money you will need in the near future.

XEQT

XEQT is 100% equities, which means you can and will see massive volatility over your investing journey. Do not panic, just ignore it. The best investors are usually though who pay the least attention to their investments. Looking at your investments grow can be fun, but it can also be painful and lead to bad thoughts when it goes down.

Just invest your money, do a once-a-year calculation to see if you are still on track with your savings goal, and then slowly add bonds as you get older (wise thought).

The less you pay attention to your investments, the better your life will be. As your account grows, it can get painful to see several months of income go up or down in a single day. However, that is the nature of investing.

I’ll give you the answer people love to gloss over whenever threads like these are asked. But it is very important for you to understand.

Robo Advisor Vs. Self-Directed

The primary reason to use a Robo Advisor (although I’d personally avoid WS myself) over self-directed broad-based ETFs is to remove the requirement of self-control from investing. Which is to say, when markets are going through a downturn, it dramatically reduces your ability to make a critical failure error (i.e. panic selling).

Let me make this clear, no one understands their ability to navigate protracted bear markets and crashes until they have experienced them. Do you think the 6-12 month period of March 2020 was a bear market? Try that, except not seeing your asset values recover for 3,4, or 5 years (see 2008-2013).

Being invested in a Robo advisor means you continue contributing on time, every time, and you don’t sell until you need the money. You can basically literally ignore all financial news and it would probably be in your best interest to do so if you’re investing long-term.

Now, is that worth the 0.5% you pay them every year? That’s up to the individual. But I’d hate to be the guy who went “Nah it’s not worth it”, and then ended up selling their ETFs for a 20% loss during the next market downturn.

Do your own due diligence but some alternatives are Questwealth Robo, ci direct (previously Wealthbar). You want a Robo solution that buys globally diversified index funds that minimize sector or regional picking while auto rebalancing according to your risk profile. You don’t want any Robo which does excessive tinkering as part of their strategy.

The reason why I specifically call out WS for this is because they very clearly tinker more with their underlying holdings than I would think is “reasonable” for a passive ETF strategy.

That is a great way to look at it. I for one feel I can handle those bear markets, but it does make it easier when you have that Robo Advisor that will continue to invest for you rather than selling at a loss in a self-directed ETF for example.

Thanks for reading! Please let me know your thoughts and comments below.

Top 10 Popular Posts Of All Time

- Top 30 Canadian Blue Chip Stocks You Should Own

- How To Use A My Service Canada Account

- How To Watch Free TV Shows In Canada – List of 10 Best Sites

- VGRO Review – Vanguard’s Best Growth ETF Portfolio

- Top 7 Canadian ETFs You Should Own

- Top 150+ Dividend Stocks In Canada – Complete List

- Credit Karma Canada Review – Free Credit Score And Report

- CPP Payment Dates – How Much CPP Will You Get?

- Top 5 High-Interest Savings Accounts In Canada

- How To Open A CRA My Account?