Bitfarms and Hut 8, both are Bitcoin Mining companies from Canada.

While Bitfarms trades at well over $6.50 CAD per share, Hut 8 on the other hand trades at almost $10.50 CAD today.

And both these companies are listed on the Canadian and the US stock markets. OTC though.

While Bitfarms is listed on the Venture Capital Markets or TSX-V, Hut 8 is listed on the TSX main market. This does make a huge difference when compared to the volume NASDAQ trades at i.e. MARA or RIOT (Bitcoin mining companies from the US).

While Bitfarms or Hut 8 (Canadian companies) have an average trading volume of 2-3M per trading day, MARA and RIOT can easily trade 10 times more at 20-30M on the average trading day. That’s the average volume and numbers these NASDAQ stocks get, on any given trading day.

Anyways let me not deviate from the main topic here, if you want to buy/switch to either Bitfarms or Hut 8 which one’s better and why I do feel so? that’s the motive of this article.

Again, I will not be getting into the market cap and other stock fundamentals, want to keep it straight and address to the point.

Let’s begin.

Bitfarms

Bitfarms is currently making 350,000+ USD per day in gross profits mining more than 9 Bitcoins per day. Or 270 BTC’s per month. That’s almost 14M per month at today’s prices.

Pros:

-

From Jan 1st, Bitfarms started Hodling or holding Bitcoins, which means that they are no longer selling the Bitcoins mined in the open market. This way they are accumulating more coins (they currently mine around 9 or 270 coins per month) over time. Currently, Bitfarms holds close to 500+ Bitcoins valued at 27M.

-

Bitfarms has an excellent management team. They are very good and vocal about their expansion plans, PR team, Twitter and social media. you can even send them a mail and get a response from the company’s president.

-

Bitfarms has better operation margins when compared to Hut 8. The price to mine per BTC is $7000 USD while for Hut 8 it’s definitely more. This impacts the gross revenues or net profits down the line.

-

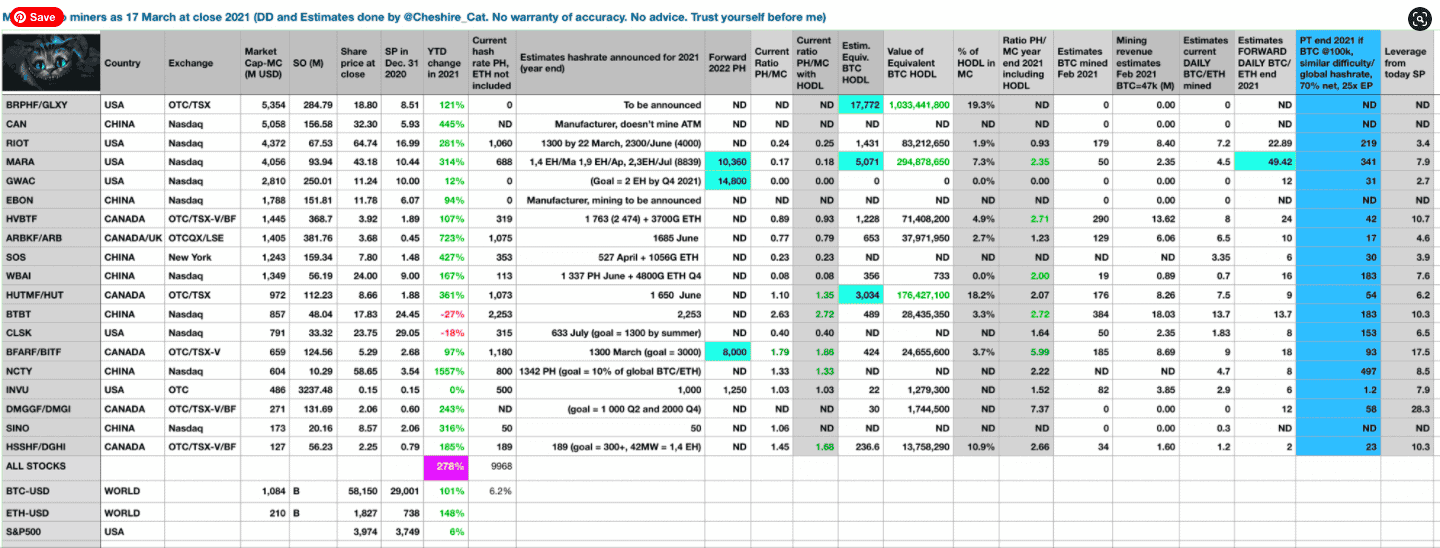

Bitfarms’ current market cap is around 600M CAD, which is extremely undervalued when compared to 1.1B of Hut 8. Though Hut 8 mines fewer coins than Bitfarms (6.7 coins per day). Bitfarms current installed hashrate capacity stands at 1.3 Ex/s.

-

Bitfarms Investor Presentation was last updated in December 2020. You can visit and download the presentation here. Just look at their expansion plans (future) and gross mining revenues/comparison to peers in a similar space.

-

No debt at all. Cleared all the outstanding debt from Dominion Capital in Q1,2021 (recently).

-

Recently appointed a PR team exclusive to the US (CORE IR), which should hopefully drive good for the company’s stock visibility and volume.

-

By the end of 2021, Bitfarms aims to be at 3 Exahash and by 2022 end at 8 Exahash (confirmed order already). Delivery of these new miners will begin from Jan 2022 all the way till December 2022.

-

200 MW huge expansion plan in South America, not sure when, but has been confirmed in the IP again.

-

Bitfarms is audited by the big 4 Canadian firms, legit website, legit photos, hashrate disclosure. Peace of mind investing.

Cons:

-

First of all, the stock trades on the TSX-V and not the TSX and OTC Markets in the US. This one’s constantly been discussed in the investment forums on when the uplisting will happen, but ETA is still an unknown ATM.

-

While Hut 8 holds more than 3,000 BTC’s currently, Bitfarms is only at 500 now (That’s because they entered the HODL game late).

-

The stock keeps getting diluted, 138M outstanding now, which will further hurt the EPS and SP down the road.

-

250M USD further dilution announced, which is good or bad, not sure, probably doing this to pay for the 5 Exahash miners ordered from Jan, next year.

-

Lots of unknowns still, regarding hash rate increases and miner purchasing to meet the 3 Ex by the end of this year. They are currently only at 1.3 Ex/s.

Hut 8 Mining Corp.

Hut 8 is currently making 300,000+ USD per day in gross profits mining more than 6.7 Bitcoins per day.

By June 2021, Hut 8 plans to increase the hashrate to 1.65 Ex/s with confirmed mining orders. Or 270 BTC’s per month. That’s almost 14M per month at today’s prices.

Pros:

-

HODL King: Though MARA (US) purchased 4,800 coins at an average cost of $31,000 USD per coin, Hut 8 has been mining BTC for several years now. All the Bitcoins that Hut holds are self-mined. Moreover, The company is continuing to add 6.7 BTC’s every day, thus making Hut 8 extremely valuable and stable in terms of producing optimal cash flow.

-

Furthermore, Hut 8 has two mining facilities – one at Drumheller and the other at Medicine Hat (Alberta). Though they have locked in electricity rates (10Q), still, the efficiency of the miners and the uptime is 99% only recently. Until now, they had much less efficiency rates.

-

Hut’s PR team (Sue Ennis) is very active on ST and Twitter handles, with one tweet/update per day. The team also adds photos/pictures of the miners, which only proves the Genuinity of the company.

-

Hut’s team is constantly coming up with something new and innovative – for example – the team recently announced that for the existing MW they have, they are replacing 1 miner with 2 additional latest Gen miners utilizing the same space and increasing the hashrate by 3X. And the same Electricity! Another recent update was that, their partnership with Validus Power Corp.

-

Simply put, the company is legit, their operations are very transparent, you can visit their mining farms and learn more about BTC mining, unlike few other scam companies out there.

-

Hut 8 is proudly Canadian, listed on the TSX and the US OTC markets, with plans to uplist in the US Shortly (no official news though).

-

The company is extremely positive in responding to the Investor’s queries, drop in a mail and you’ll for sure get the response back or you can reach out to Sue on ST at bigsuey. She is very prompt in answering the unknowns.

Cons:

-

Stock dilution is the problem again. Just like Bitfarms, Hut 8 too constantly keeps liquidating its stock. Currently, they have around 113M outstanding shares, and they are planning to dilute up to 500M USD more over the next 2 years (500M USD/$8 per share price today). The reason for this dilution can further be accounted to the insane rise of the BTC price. So, gradually all these miners want to buy more machines, plan further expansion and so comes the liquidity (Coz remember they are all holding the coins they mine, the more you hold – the more you make when the coin price rises).

-

Hut’s operating margins to mine a Bitcoin is way higher than Bitfarms. In fact Hut 8 hasn’t disclosed their exact rate to mine per coin. In the case of Bitfarms, it’s $7000 USD, MARA $4500 around. Not known for Hut 8.

-

Hut’s stock volume is extremely low similar to Bitfarms, as compared to the US mining stocks.

-

Unlike Bitfarms, we have no clue about Hut’s future expansion plans. Bitfarms has already committed for the hashrate increase to at least 3 Exahash by the EOY and 8 Exahash by the end of next year.

So Which One’s Better: Bitfarms or Hut 8?

Huge thanks to Chesire_CAT from ST.

Hut 8 currently has 3012 bitcoins in its inventory. And all those coins are self-mined.

Moreover, Hut 8 is on the verge of announcing its quarterly results next week i.e. on March 25th, 2021. So, the revaluation gains alone for the 2800 coins (as per the previous quarter) should be close to 60M USD. That’s apart from the mining revenue.

Now consider this, for the next quarter (Q1, 2021), Hut 8’s revaluation gains will be 3012 coins*(60,000-29000) = 3012*31000 or around 90M just from the revaluation gains alone.

And, now that Hut 8 doesn’t have any outstanding loans or debts, plus with their 4% yield gains with Genesis, plus the increased hashrate to 1.3 Exahash/second, and with BTC prices rising, sky is truly the limit!

Talking about Bitfarms, they only started hodling the Bitcoins from the beginning of Jan 1st, 2021.

Though they are late to the HODL party, since then, they have already accumulated around 500 coins now which is worth close to 30M dollars.

Remember, Bitfarms currently has the same hash rate as Hut8 at 1.30 Exahash and their operations are better than Hut 8.

Moreover, Bitfarms is the most undervalued stock trading at around $6 CAD (see the above chart for the machine/ph comparison).

For reference, Hut 8 currently trades around $10.50 CAD.

To conclude, I believe that Hut 8 is the better choice when compared to Bitfarms today. The main reasons are their bitcoin holdings and the partnership with Validus.

Hut 8 Q4 & Forward Projections

Bitcoin owned on Dec 31 – around 2950.

Revaluation 10K to 30K = 60 million profit.

Bitcoin Mined around 6million profit for the quarter.

Total profit quarter 66million USD.

Price Hut 8 900million USD.

900/66 = 13,6PE for the quarter. which is 3.4 Annual PE at this rate. Considering the average Industry PE at 25, this one should 7X from here.

Next, why I am bullish. As Jaime Leverton, CEO said on one of her latest podcast’s their miners have a span life of 2 years written on the balance sheet (this is very conservative) so a lot of their miners are written off as useless while being still in use (and making a profit). This makes their balance sheet in itself very very strong.

Third – The flare gas expansion will give them power at the absolute lowest price in the future, which will make the company profitable at mining at any state of the bitcoin cycle. Crypto winter mining prices are no problem when ur mining for almost free.

Fourth, Hut 8’s BTC (3000+ coins) on the balance sheet generates interest. They lent it out to other people which gives them a revenue stream in Fiat, making them able to pay a portion of their expenses, which results in more HODL over time.

Fifth reason, Hut 8 is one of the largest publicly traded BTC holders. After mining is no longer as profitable in 10 to 15 years (say), they can act as the new age BTC bank, which will make them a financial company.

Finally, NASDAQ listing will come and is imminent. They are not stupid. Hut8 has done everything one step ahead of the competition. The management team is insanely good at what they are doing.

Bitfarms Future Hashrate And Profitability

With Bitfarms, since they did not HODL any coins for the q4, they are most probably going to be negative in earnings. That’s considering depreciation, loan, interest and electricity costs. BTC was at 29K USD on 31st Dec 2021 (Q4 end).

But for the next earnings (Q1, 2021) with the hash rate increase and the current Bitcoin price sky is the limit for the SP.

As I mentioned earlier, Bitfarms is into holding BTC now. With over 200 coins per month, which equates to more than 10M added to the balance sheet on top of their incredible mining costs of 7K per coin.

Bitfarms already has a commitment for 8 Exahash by the end of 2022. And 3 Exahash by the end of 2021, which equates to 20+ Bitcoins per day mined. (at current difficulty levels and 3Ex/s).

Thanks for reading, please let me know your thoughts and comments below.

Top 10 Popular Posts Of All Time

- Top 30 Canadian Blue Chip Stocks You Should Own

- How To Use A My Service Canada Account

- How To Watch Free TV Shows In Canada – List of 10 Best Sites

- VGRO Review – Vanguard’s Best Growth ETF Portfolio

- Top 7 Canadian ETFs You Should Own

- Top 150+ Dividend Stocks In Canada – Complete List

- Credit Karma Canada Review – Free Credit Score And Report

- CPP Payment Dates – How Much CPP Will You Get?

- Top 5 High-Interest Savings Accounts In Canada

- How To Open A CRA My Account?